Investors in Apple have had an un-Apple-like year, but at least one analyst thinks that will change in 2023.

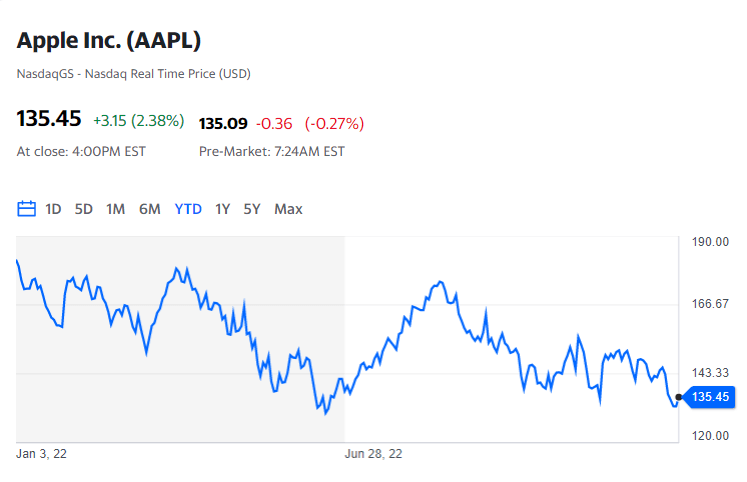

The tech giant’s stock has dropped 25% in 2022, lagging the S&P 500’s 19% drop.

The decline comes despite Apple often being viewed as a safe-haven investment, as it boasts a formidable balance sheet flush with cash and a steady stream of repeatable services income.

But just like other large companies, the volatile global economic backdrop has hit Apple in the form of slowing iPhone and accessory sales, as well as production delays out of COVID-19-stricken China.

Apple’s stock now trades on a forward price-to-earnings ratio of 22, a roughly 21% discount to its historical average. At 16 times forward enterprise-value-to-EBITDA, Apple’s stock trades at a 17% haircut to its historical norm.

The more compelling valuation on mighty Apple has caught the attention of long-time tech analyst Jim Suva at Citi.

“We believe demand for Apple’s products and services is likely to remain resilient throughout FY23. We do recognize that regulatory risks remain a major overhang on the stock, but we view these as headline risk rather that fundamental risk. Such headlines could provide a near-term stock pullback which we would view as a buying opportunity for Apple shares,” Suva wrote in a new 20-page report to clients.

Suva reiterated a buy rating on Apple with $175 price target, which assumes about 30% upside from current levels.

Added Suva, “Apple’s current market value does not reflect new product category launches. This will change with the launch of the new AR/VR headset in 2023 and foldables in 2024.”

Here are the six factors behind Suva’s bullish 2023 call on Apple.

- Here comes India: A little appreciated factor in Apple’s future growth is India, Suva says. The biggest bullish factor on India, Suva says, is the growing wealth of the country’s population. “India’s upper-mid and high-income middle class, with incomes of $8.5K+, is expected to double from currently representing 25% of its households to more than 51% of total households (~200 million). These households are expected to increase spending by six times from representing 37% of current spending ($1.5 trillion) to 61% of $6 trillion by 2030. Middle-income and high-income households would drive nearly $4 trillion of incremental consumption spend by 2030. Overall, there will likely be nearly $2 trillion of incremental spend on affordable, mid-priced offerings, in parallel with $2 trillion incremental spend led by consumers upgrading to premium offerings or adding new categories of consumption,” Suva says.

- iPhone sales growth: Suva says sentiment on iPhone demand has gotten too bearish. “Investor sentiment across consumer tech hardware is very dour, with many believing that the strong growth seen overall in iPhones over the past two years (+23% revenue compound annual growth rate) is likely to see sharp declines ahead as macro inflationary pressures take a bite out of consumer spending. We do not believe this is the case, in other words, we do not expect a repeat of FY2016 or FY2019 when revenues declined by ~10-15%,” Suva writes. The analyst uncorks several reasons for his more optimistic view. “Our view is that the installed base of Apple’s iOS ecosystem is significantly larger now, implying an installed base at 1 billion plus iPhone users. Additionally, our research does not indicate smartphone replacement rates are lengthening (compared to recent levels) and are holding steady, and in some cases even shortening overall,” Suva adds.

- Services sales upswing: Suva’s research shows Apple’s services sales growth has cooled in 2022, in part due to a slowing economy. But that may change in 2023. “We expect price increases that were implemented in the last quarter to take effect in the ensuing quarters and will drive revenue growth ahead,” Suva says on the services business.

- Those new products: “We expect Apple to launch an AR/VR headset in 2023,” Suva says. The analyst points to improvements in 5G connectivity and a competing offering from Meta’s Oculus as key reasons Apple will finally enter the market. Any product announcement along these lines could propel the stock, Suva thinks.

- Regulatory risk overblown: Recent reports contend that to comply with the Digital Markets Act in Europe, Apple may allow alternative app stores on its iPhones and iPads. Suva believes the impact to Apple’s dominant app-store business is overblown. Says Suva: “In our view, there are several factors that may limit the impact from these off-store billing options including consumer behavior which in our view tends to be sticky, especially as it relates to the ability to securely pay and manage their subscriptions in one place.”

- The cash giveaways: Suva thinks Apple is poised to drop the mic when giving cash back to investors next year. “With free cash flow of ~$110 billion plus per year and net cash of $49 billion (as of year end FY22), we expect Apple’s cash chest to support at least $110 billion plus in shareholder returns per year, amounting to 4-5% of its current market cap in the form of buybacks and dividends. In spring 2023, we expect Apple to announce an incremental stock buyback of $85 billion after deploying ~$90 billion in FY2022. We also expect the company to raise its dividend by 10%,” Suva writes.

Source: finace.yahoo.com