Stocks mounted an impressive comeback Wednesday, with the Nasdaq Composite (^IXIC) nearly erasing its biggest opening deficit since October. The Dow Jones Industrial Average (^DJI) eked out a small gain — its fourth straight — after spending most of the day in the red.

Even Microsoft (MSFT) rallied back from a 4.6% early loss to end the day down only about half a percent.

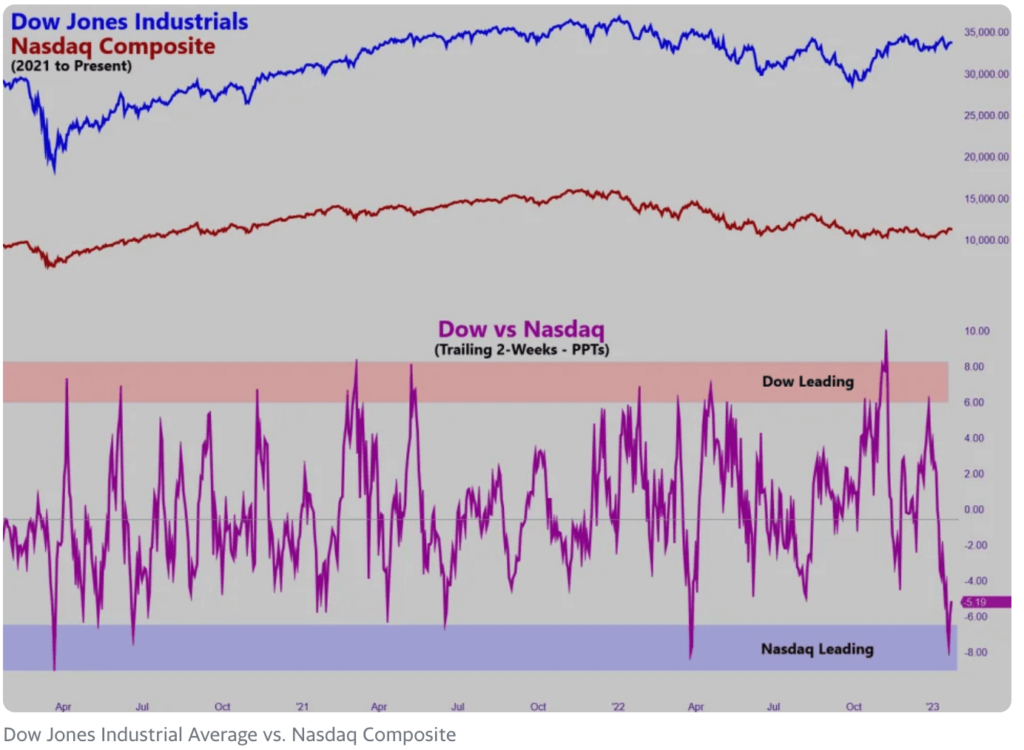

This year’s market action has been a reversal of one of last year’s most important trends, which saw the Dow outperform the Nasdaq by the widest margin in two decades.

This year, the Nasdaq is now up 8%, substantially outperforming the Dow’s return of just under 2%.

And while it’s unlikely a new bull market led by tech has begun, this relative performance is a tantalizing reminder of the gains tech bulls reaped in growth stocks during the ultra-low interest rate regime that had prevailed since the Global Financial Crisis.

And with several benchmark indexes right now at key levels, a squeeze out of current trading ranges would likely generate upside momentum.

First, take a look at the highly cyclical semiconductor space, where the PHLX Semiconductor Index (^SOX) is attempting to break out of a 9-month long inverse head-and-shoulders technical formation.

A breakout higher would suggest bulls retaking control after bears dictated price action for most of 2022.

If the majors follow suit and manage their own respective technical breakouts, those moves would likely generate significant momentum given the duration of the consolidation under current levels. The longer an index, stock, ETF, or any other traded asset consolidates around a particular price level, the stronger moves tend to be when the price breaks higher or lower.

For the S&P 500, the December highs around 4,100 mark the upper end of the current range; the index closed at 4,016 on Wednesday.

Meanwhile, Nasdaq has been constrained by 11,500 on the upper end since September, while the Dow has been stuck under 34,500 since April. These indexes closed at 11,313 and 33,743, respectively, on Wednesday.

However, it would be slightly unusual for risk markets to simply rally from here given how stretched the Nasdaq is versus the Dow — as evidenced by the below chart, which dates back to the beginning of the pandemic.

The Dow’s weakness in the face of Nasdaq strength this year appears to have reached a short-term extreme, and is in the process of reversing. And extreme readings have tended to coincide with short-term highs in stocks since the bear market got under way last year. However, during the pandemic bull market of 2020-2021, these extreme readings of relative outperformance tended to do little to dent the rally.

So, if the major indexes do roll over from here, tech and growth stocks would likely sell off more than cyclical and defensive names, allowing the Dow’s performance relative to the Nasdaq to normalize in the short-term. For those concerned with news and fundamentals instead of the technicals, the narrative to explain this price action would likely fixate around a hawkish Fed, higher rates, and disappointing earnings du jour.

Conversely, if chip stocks and the big benchmark indexes rip higher through current resistance, that would likely send the Dow-to-Nasdaq ratio sinking far below its current level.

The bottom line is that stocks could very well surge from here, and the technical setup suggests we’re a crucial juncture for this year’s market rally.

But any rally led tech stocks is likely to be fast, furious, and short-lived.

Otherwise, markets will need to consolidate and save energy for a more durable move higher another day.

Source: finance.yahoo.com